A couple of months ago, more or less on a whim, I started sinking $50 a week into Bitcoin.

Yeah, I know. Stay with me here.

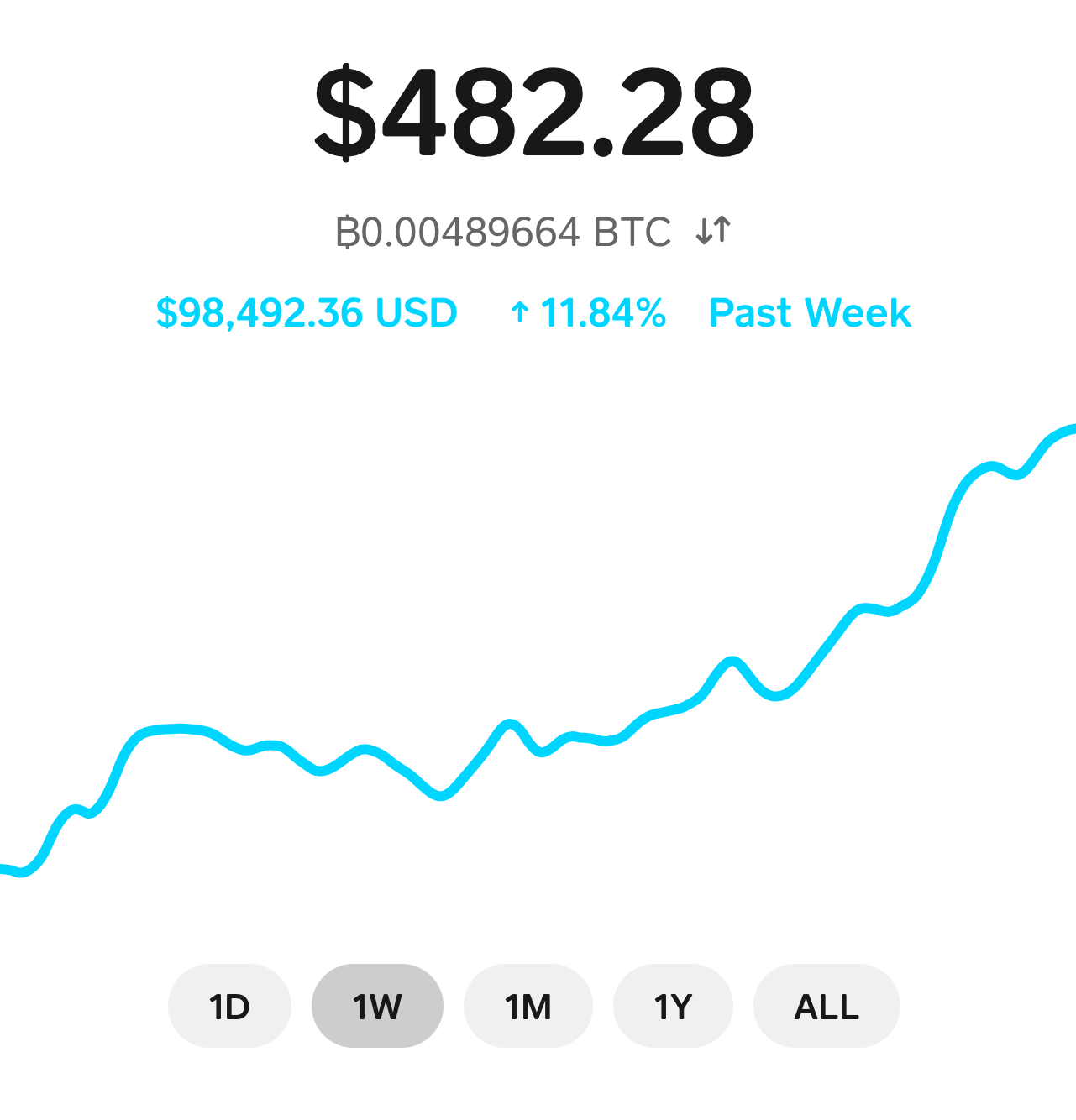

You are not reading that incorrectly.

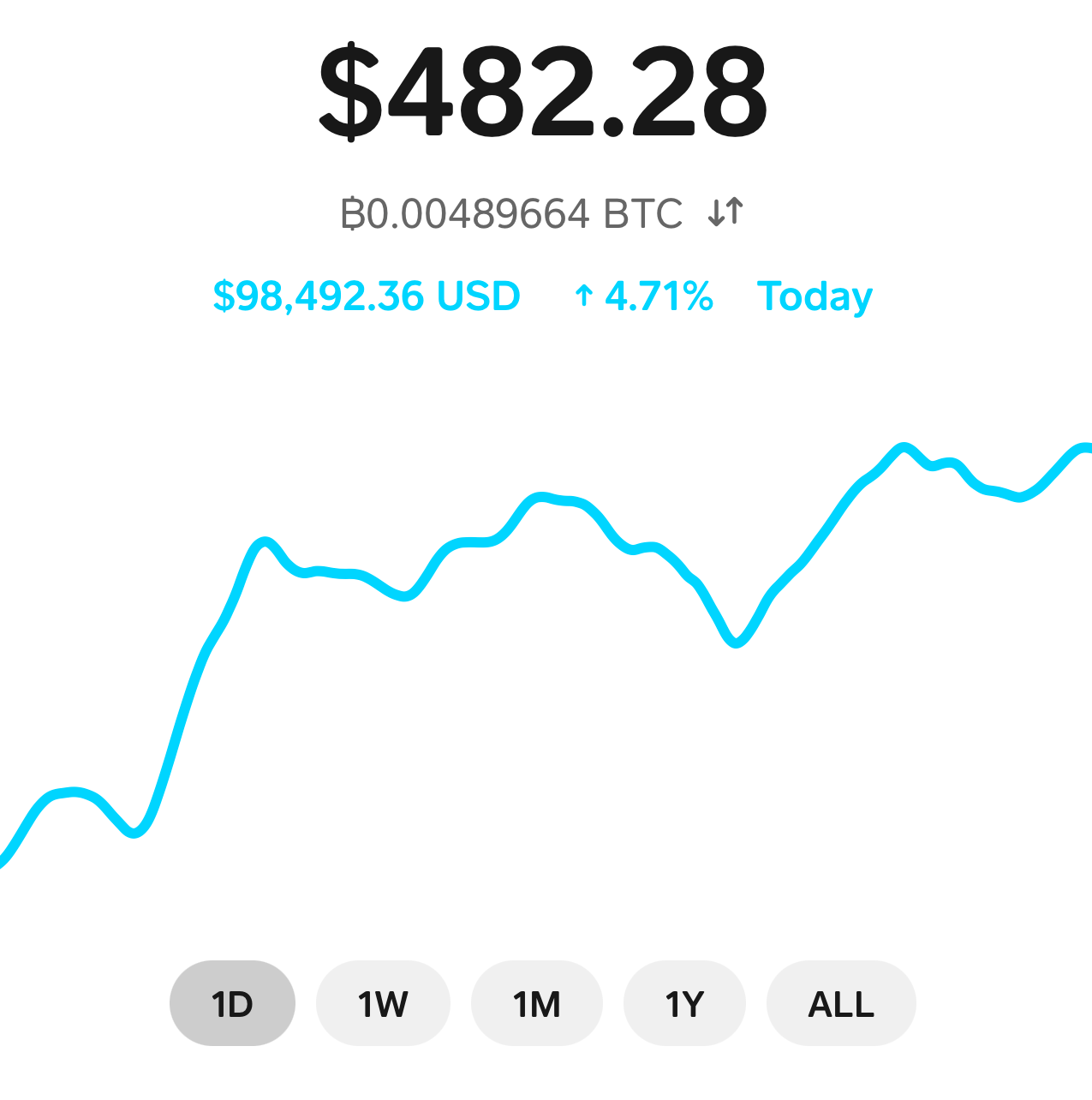

That is up nearly five percent today, nearly twelve percent this week, and nearly fifty percent in a month. Those are fucking insane numbers. Ridiculous numbers. Stupid numbers. “That can’t be right” numbers.

I have actually invested $342.16. My personal actual rate of return over the last seven weeks or so is 40.9%. I assume there would be some transaction fees or something and taxes to set aside once I sell, but that’s ludicrous.

I am seriously and genuinely considering getting a zero-APR advance from one of my credit cards to sink into Bitcoin for a month, at which point I’ll sell off whatever the advance was, pay it off, and let the profits coast for a little longer. I’m not talking about an enormous amount of money, relatively speaking; nothing that would bankrupt me or even put me into real trouble if the market crashes, and one way or another I probably want out of this (or do I?) before Trump takes office and wrecks the economy. But 40% of, say, $5000 is two thousand dollars in a month. Even if the rate of return drops by half that’s still a thousand dollars for doing nothing. When I started thinking about this a week or so ago, the one-month number was around thirty percent.

There’s got to be a correction of some sort coming soon, right? Nothing stays on this high of a trajectory for long, and Bitcoin is proof positive that money (and the investment market) is nearly entirely fake anyway. But … shit.

Am I gonna end up $2,000,000 in debt in two years, and this is the post that led to my downfall?

Somebody tell my wife about this post so she can forbid me to invest in this stupid, imaginary product, please.

Nevin Longenecker, my freshman Biology teacher, passed away last week. I was surprised to realize, when I checked, that Mr. Longenecker was not among the teachers who I dedicated Searching for Malumba to. I can sort of reconstruct my logic; every high school teacher I mention on that list was someone who I spent at least multiple years if not all four years of high school with, and I only had the one class with Mr. Longenecker. Among his many accomplishments as an educator was his senior Research Biology seminar, an opportunity that several of my friends participated in and which, over the years, generated literally millions of dollars in research grants. I was not planning on a career in the sciences, so I was not part of that seminar, and Mr. Longenecker’s direct role in my education ended after my freshman year. He was, regardless, one of the finest educators I ever had the pleasure of being in a classroom with.

He started teaching at my high school in 1968. And Adams wasn’t his first school. He taught for sixty-four years in total, and never actually retired, although my understanding is that health reasons prevented him from starting this school year. He started that research program in 1976, the year I was born.

Sixty. Four. Fucking. Years. I am a grown-ass man with white hair and I have sixteen years to go before I have lived as long as he was a teacher. Fifty-six years at the same school, and I’d bet money that hewas still in the same classroom that he occupied when I was there. I’m trying to imagine the pressure of being the next person to move into that room and I can’t do it.

The phrase “rest in peace” has had all the edges rubbed off of it by years and years of use, but I cannot imagine someone who deserves more peace and rest than someone who taught high school for six and a half decades.

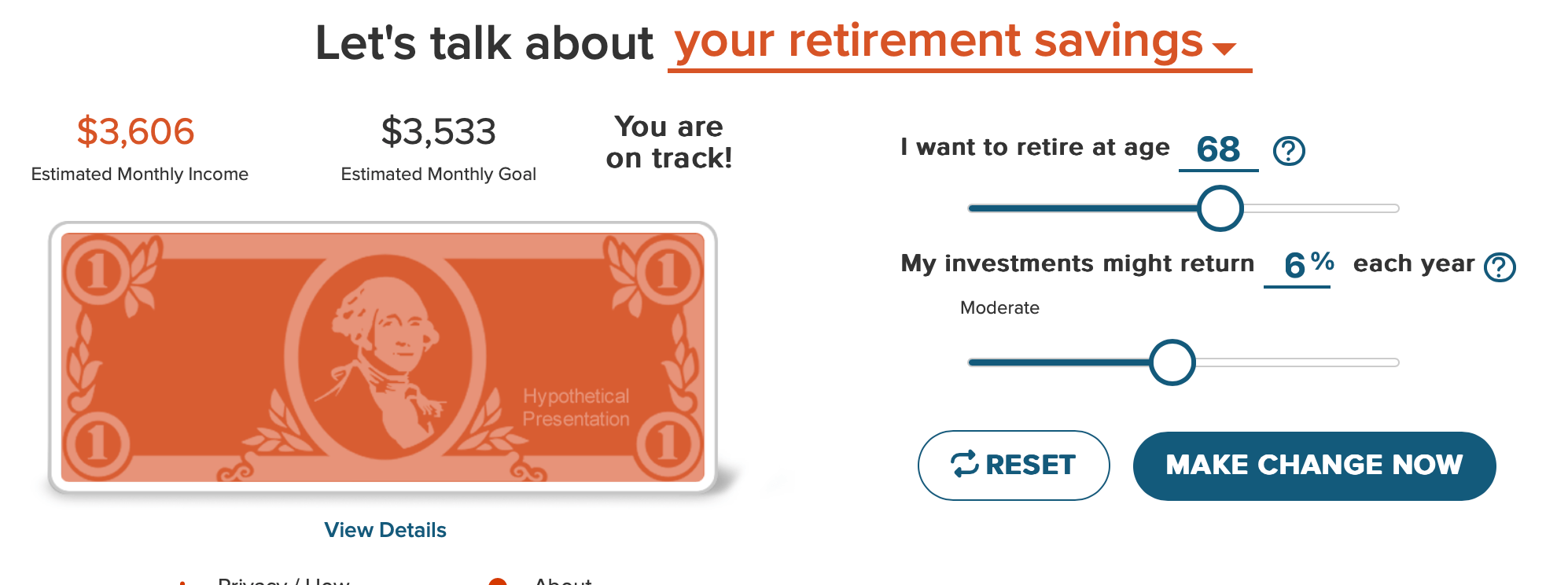

Meanwhile, and the reason this isn’t headlined as an RIP post, I logged into my pension website and was greeted with, I believe for the first time, an indication that I was hitting my “retirement goals.”:

I don’t know who generated that $3533 number, for the record, or how or if it’s slid around during my years as an Indiana teacher, but this is the first time that dollar bill has been entirely orange. I don’t want to hear shit from anybody about how bad the economy’s doing; apparently my retirement account is up sixteen percent this year, which is ludicrous. I can’t even move that “might return” slider far enough to the right to account for sixteen percent increases (and, okay, I know it’s not going to last forever, too, but still.)

Anyway, I was happy for a minute, until I saw that retirement age.

68? Sixty-eight? Sixty-eight???? Shit, I’m not even going to be alive at 68 much less wait that long to retire. It turns out that if I play with that slider I can earn an impressive $55 a month if I retire next year, and the magic number appears to be 62, where the orange bar makes a big jump over to the right. That’s still fourteen years out, which feels kinda crazy.

I learned all of this and had all of these thoughts before learning of Mr. Longenecker’s passing. There’s no obituary yet and I’m not sure when he was born, but if he started teaching straight out of college he’d have to have been at least 85. The craziest thing is he was the teacher with the second longest tenure in the district. As far as I know, Bev Beck is still in the classroom.

(For giggles, take a look at the article linked on that page about the “80-year-old teacher” suing the district for age discrimination, and then look at the date on the article.)

I will, nonetheless, not be aspiring to equal either of those people’s feats. That said, I probably ought to start buying lottery tickets.

Sometime in February of 2020– I could have sworn I posted about it, but hell if I can find it– I applied for a $30,000, six-year personal loan through Discover. I used the funds to pay off about 90% or so of my credit cards– so, to be clear, someone handed me thirty grand and that wasn’t enough money to pay off all of my credit cards. The payments on the loan were considerably less than the combined payments on the cards, by around $300 a month, if I remember correctly.

In September of 2021, I got that last piece of credit card debt paid off, giving me a $0 credit card balance for the first time since my freshman year of college. It probably put around $150-200 a month back into my pocket.

Two years later, aided by that extra $300 and a few stimulus payments from the government that I didn’t need because I’d been able to keep my job and work from home, I paid off my car, a full year early. Another $237 a month went back into my pocket.

On May 9th, 2022, my student loans– nearly $70,000 worth– were forgiven through the Biden administration’s Public Service Loan Forgiveness program. Another $545 a month went back into my pocket. I started paying a thousand dollars a month, sometimes more if I could afford it, on the personal loan, which had a monthly payment of $607. The entire time I was paying off the loan, I never made a single payment for just the amount that was due.

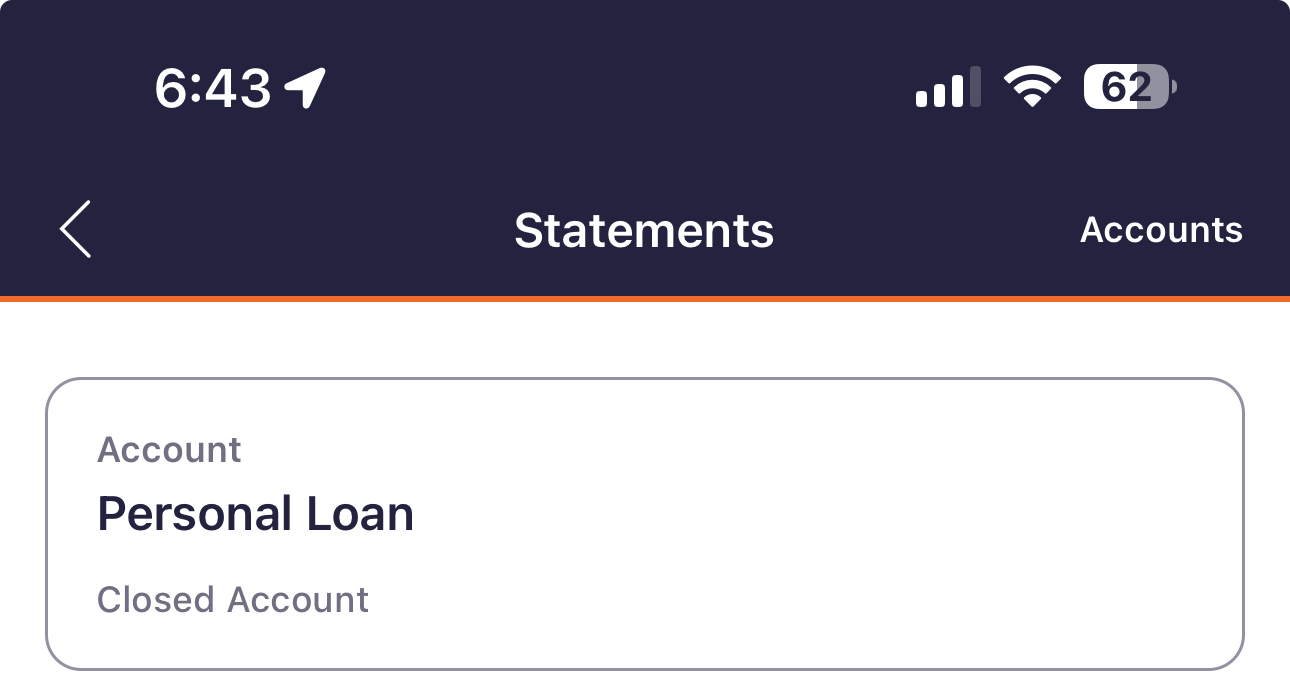

I have been watching a little bar crawl across the screen of my phone over the last four years as that personal loan got slowly whittled down. Last Saturday, I made my final payment of $756, and then reloaded the app about a dozen times an hour for the next few days, waiting for it to update and show me that the loan was 100% paid off. I was looking forward to the screenshot.

Turns out when you pay off a personal loan, which I did almost two full years early, they just … close the account, which feels kind of anticlimactic.

Other than a small installment loan through Apple that I will pay off on the paycheck after next, my mortgage, and a home equity loan that we used to remodel the bathroom– and to be honest, for some reason I don’t even feel like the home loans count, I am now completely debt-free.

No student loans.

No credit cards.

No personal loans.

No car payment.

A thousand bucks a month now back in my pocket.

If I was a Republican, I’d already be writing my personal finance book, talking about how my good financial decisions and iron self-control led me to shake off a lifetime of bad habits and Get Out of Debt.

That is not what happened.

The fact is I’ve been incredibly lucky.

I was lucky enough to be back in education when Covid hit. If I’d still been a furniture salesman, I’d have been fucked.

I was lucky enough to be married to someone who both handles her money better and makes more than me, so I wasn’t trying to pay for my entire household on my salary and could devote large chunks of it to debt relief.

I was lucky enough that the government sent me Covid relief checks that I didn’t really need and could devote to debt relief.

I was lucky enough to qualify for President Biden’s improvements to the PSLF program, which I had tried to take advantage of several times before and hadn’t been able to for one reason or another.

I was lucky enough to have a good-paying union job that provided me with a steady paycheck and yearly raises that, for the most part, I also didn’t really need, and lucky enough to get hired by a higher-paying district when I left South Bend schools. Most of that extra money went to debt relief.

I was lucky enough that my family has largely avoided any sort of financial crises over the past four years– no sudden illnesses or injuries, no major accidents, no natural disasters, fires, thefts, or anything else that could have suddenly laid claim to who knows how much of my money. One bad car accident and I could be millions of dollars deep into medical debt instead of being practically free of it.

I have been very, very lucky. And while I’m not going to sit here and tell you I’m never using a credit card again– they’re fucking useful, that’s why they exist– I’m hoping to never have to dig myself out of that hole again.

But one way or another, this week, I’m celebrating. Celebrating, and trying my damnedest to not run out like an idiot and spend myself right back into a hole again. I’m not buying a car until the boy turns 16 and gets his license, and provided that nothing stupid has happened in the meantime, he’ll inherit my current car at that time. So I’ve got four years– three and a half, really– to take that surplus and invest the shit out of it. If I stay lucky, the market will continue on its current trajectory, and maybe I’ll get to retire before I die.

…and then ruin them by relating them to Dungeons and Dragons.

Folks, as of today, technically, and definitely as of Saturday when the payment will officially go through, I have no credit card debt. This has not been true at any point since I was in college– probably since my freshman year, in fact. Said credit card debt was at one point north of thirty thousand dollars and it is now gone. Now, I’m not free of debt itself by any means– there is a mortgage, and a car loan, and my student loans, and another installment loan at a very low APR that I used to make a large chunk of that credit card debt not credit card debt any more. But this is still a Goddamn milestone; I don’t owe any money to actual credit cards any longer, and every debt I have is on an installment plan where I can point at a date on a calendar and say “This is when that will be repaid.”

Except not really, because now that I’ve got the money I’ve been using to aggressively pay down credit card debt back in my pocket, I’m going to start working on the car. I think I can actually afford to make my car payment twice a month now and still come out ahead from what I was putting into credit cards. That’ll have that paid off in a little over a year, I think. After that, assuming I don’t lose my job or have some other shit life event, things are going to seriously change. I will be moving into Actual Discretionary Income territory, which … well, I know it probably seems like I already spend money whenever I want to, and yes, I’m saving up for a criminally expensive lightsaber as a Paid Off My Credit Cards award, but … this is still a big Goddamned deal, y’all.

I just gotta remember to spend the rest of my life not being stupid now.

First, that it is 7:30 PM, and I probably ought to blog today;

Second, that I am officially closer to retirement than I am to college, even assuming I wait to 65 to retire;

Third, that my student loans are due to be paid off four years prior to said 65th birthday, which should be a crime;

Fourth, that even if the notion of living another 20 years much less teaching for that long is difficult to wrap my head around, I probably ought to take this retirement thing seriously since I have, y’know, a wife and child in the mix now.

In case you can’t tell, I met with a retirement … dude, of some sort, at work on Friday, and several mortality-confronty sorts of things were discussed, and then this weekend I managed to keep my shit together long enough to dig through the folder that I throw anything even vaguely investment-related into and find not one but two different investment-related accounts that appear to no longer be receiving active contributions; I did some strategic scanning and sent them off to The Dude with a note attached that basically said I don’t know any of the money words, please help and we will see if anything happens. I have never really believed in retirement, to be honest; not in the sense that I don’t want to eventually quit working– I want to quit working now— but in the sense that I suspect any money I “invest” in my “future” will be stolen or siphoned off somehow before I’m able to actually benefit from any of it.

Today also included mowing, putting all my laundered clothes away like a big boy, finishing a book, starting another one, getting my grading done, writing a number of important emails, and a couple of videos recorded for The YouTubes. All in all, not bad for a Sunday.

In the past time-has-no-meaning-anymore-so-let’s-say a month or so, I have developed and abandoned several new hobbies. I was super into woodturning for a while, and recently I’ve developed a fascination with paper- and bookmaking. I have turned no wood, made no paper, crafted no books, but I’ve been watching a lot of videos. I’ve managed to avoid spending any money on anything, although the fact of the matter is investing in the few things I’d need to make some shitty little notebooks with my copious spare time and brain cycles would actually not cost very much.

The other day I discovered that an app I was already using for something else allows me to buy stocks and Bitcoin. On a lark, and because I’m so unused to the concept of having spare funds that I don’t know what the hell to do with it, I bought $20 in Apple stock and $20 in Bitcoin, and at some point in between then and now I bought $25 in Moderna stock and upped the Apple buy to $25 so that they were even. Because that is how you make stock decisions; you look at how much you’ve spent on two entirely different companies and even the amounts out just for the hell of it.

Bitcoin has plunged in value since I bought it. Like, to the point that there are articles being written about it. I’ve made like two bucks on the stocks. But the fact is, I don’t know anything about any of this and in theory I would like to retire some day, so … maybe I should learn something about how, like, investments work? When I was unemployed a few years I had to cash out what little retirement I had so we could, like, keep the house, so in theory I have some investments in some funds somewhere and some retirement accounts, maybe something with a K in the name of it or something, although it’s not a 401K because something something public employee, I don’t know. But I don’t know anything about this.

(An example of how little I know: I found out earlier that a Pfizer … subsidiary … named BioNTech may be close to a Parkinson’s vaccine. I don’t know what a subsidiary actually is or whether BioNTech is one, but the companies are related somehow. BioNTech is BNTX on the Nasdaq and the app I’m using appears to not know it exists and I don’t know why, because I don’t actually really know what the Nasdaq is, or if it’s different from what I’m using to invest, and blah blah blah blah. I do not actually really know what “The Dow” is, in any functional way, other than it seems to be a graph that reacts to the emotions of rich people on any given day. I’m real real real dumb about this. I need to be less dumb, so I need a way to learn.)

So here’s my question, if there’s anyone out there who knows a useful amount of information about this: if I were to want to fiddle with the idea of being a small-time investor for a little while, making the occasional trade to the tune of, like, $20-25 a week or something like that, what apps or services should I be looking at for something like that? Ideally with a portfolio that has independent existence outside the app, so that I can take it with me, so to speak? The Bitcoin thing isn’t something I’m dedicated to, and I’m fine with the idea of selling everything I’ve bought in this app before moving to another one– I’m using such small amounts of money right now that even if I took a hit on it it’s not a thing I’m worried about.

Also, before you say anything, yes, I understand that right now is probably not a great time to get into the market, what with the impending civil war and all; again, I’m just dipping my toes in and only putting in money I’m willing to lose. I’m not about to suddenly invest an entire paycheck and cross my fingers that I’m going to get rich or something like that.

WARNING: Ill-informed rant ahead. More so than usual, yes.

Shut up.

I got another quarterly statement from MetLife today. I have something called a 401A. I phrase it that way not because I’m trying to be cute or lead into an explanation but because I really don’t have the vaguest idea what the shit a 401A actually is. I know it has something to do with retirement and I know that it is pathetically small; I’ve supposedly been paying into this thing (or maybe someone else pays into it, I dunno) for, what, seven years now?– something like that, and the total amount in the account is still less than the amount of a single paycheck. They helpfully inform me that I can look forward to a monthly retirement income of $64 (that’s not a typo) based on what I have in my account.

I have some other account with some other company; it has even less money in it. I think I started paying into that in Chicago, maybe, and then I left that job but I still have the account? I should probably “roll it over” into something; I hear that money can be “rolled over” in some circumstances and I think maybe this might have something to do with that.

And then there’s my TRF, or Teacher’s Retirement Fund. Off the top of my head I have no idea how much is in that or what it’s good for, but if I’ve gotten my quarterly report from MetLife I’m probably due to get a statement from them soon too.

That, right there, constitutes the entire sum of both my knowledge of how investments work and the current state of my “retirement fund.” I just actually tried– I think about this every time I get a quarterly statement, but this time I actually did something about it– to log into MetLife’s website to see if I have the option to be “more aggressive” (that’s a money thing, right?) with how they’re allocating my money, because the $8 that my fund increased in value over the last quarter seems… paltry.

The site is insisting that I give them my PIN. I don’t have a PIN, or at least I don’t think I do; I’m certain I’ve never logged into the website before. I clicked the button helpfully labeled “Lost your PIN?” and they have informed me that they’re mailing it to me. Because it is 1986.

Here’s the thing: I know, intellectually, that I probably ought to care about and be paying close attention to this stuff. I also know politically that my generation is not going to be allowed to retire. That’s an illusion; retirement is basically done as a concept in American society for anyone under 40. That TRF money? I’ll eat my own dick if that’s still available to me in any meaningful form when I’m 65, or 70, or whatever age they think I ought to be working to by the time I supposedly get to be that old. That shit’s gonna be stolen, no doubt by some rich ratfucker who deserves it more than I do. It’s funny money; I don’t believe for a second that it’s actually real or that it will ever actually make its way to me. I don’t particularly trust the 401A either, for much the same reasons.

I’d like to increase the amount that is getting put into this 401A plan (the corp is kicking in a contribution– at least, I’m pretty sure this money is coming from them, not me– but I’m pretty sure I can tell payroll to pull more out for it if I want) but the state legislature has made it their goal over the last several years to make sure that no teacher in Indiana ever gets a raise again, and so it’s not like there’s extra money becoming available that I could dedicate to investments.

I think I’ll go buy some lottery tickets. Or– ooh! A Bitcoin!